Sales of previously owned homes were unchanged from the month before in August, according to new data from the National Association of Realtors. The number of available homes for sale was also flat, with unsold inventory at a 4.3-month supply at the current sales pace. But, though there was little change in the numbers, Lawrence Yun, NAR’s chief economist, says buyers may be getting ready to move. “Strong gains in the Northeast and a moderate uptick in the Midwest helped to balance out any losses in the South and West, halting months of downward momentum,” Yun said. “With inventory stabilizing and modestly rising, buyers appear ready to step back into the market.” In other words, though there hasn’t been a significant change in conditions, there is a sense that price increases and low inventory are beginning to move in the right direction. This can be seen in the regional results, which show that some areas are improving at a quicker pace than others. Another indicator that relief may be on the way is how long the typical property stayed on the market in August. That’s because, the number of days homes were available before selling moved up for the first time in months. But, despite the improvement, properties are still selling quickly. In fact, the typical home sold in just 29 days in August. More here.

Financial Security Boosts Housing Sentiment

It’s said that there are two sides to every story. But there are also two sides to the calculations potential home buyers undergo when deciding whether or not it’s a good time for them to look for a new house. After all, buyers have to take into consideration the cost of homes in the areas they’re looking to live but also their own financial security. That’s why Fannie Mae’s most recent Home Purchase Sentiment Index is encouraging. Because, though Americans have concerns about housing affordability, they are feeling confident financially and secure in their jobs. In fact, the number of survey respondents who said they aren’t concerned about losing their job rose 15 percent over the month before and those reporting that their income is higher than it was 12 months earlier hit a new survey high. Doug Duncan, Fannie Mae’s chief economist, says Americans are feeling the effects of a stronger economy. “Consumers are attuned to the divergence between the slowing housing market and strong macro economy,” Duncan said. “Consumers were less optimistic this month about both home buying and home selling conditions, while perceptions of income growth and confidence about job security are at survey highs.” More here.

Why Are Younger Americans Buying Fewer Homes?

In recent years, there’s been a lot of discussion about millennial home buying preferences. Mostly, this is due to the fact that first-time home buyers have historically made up about 40 percent of the home sales in any given year. And, because they account for a large number of the homes sold each year, any fluctuation in those numbers is notable. That’s why Freddie Mac recently took a look at why the homeownership rate among young adults has dropped 8 percent since hitting its peak in 2004. As you might imagine, there are a variety of reasons for this. Among them, affordability, not surprisingly, ranks highest. Concern about being able to afford homeownership is always an issue for younger buyers. But there are many other factors that have played a role in suppressing buyer demand among first-time buyers. Some of the other common reasons named included lower marriage and fertility rates, student-loan debt, borrowing constraints, and a preference for urban living, which tends to be more expensive. In short, young Americans – in addition to affordability challenges – have more debt and are starting families later in life. But, though lifestyle and demographic changes have influenced buying activity, Freddie Mac predicts homeownership rates will rebound, if the economy and wages continue to improve. More here.

Are Unequal Housing Markets Good For Buyers?

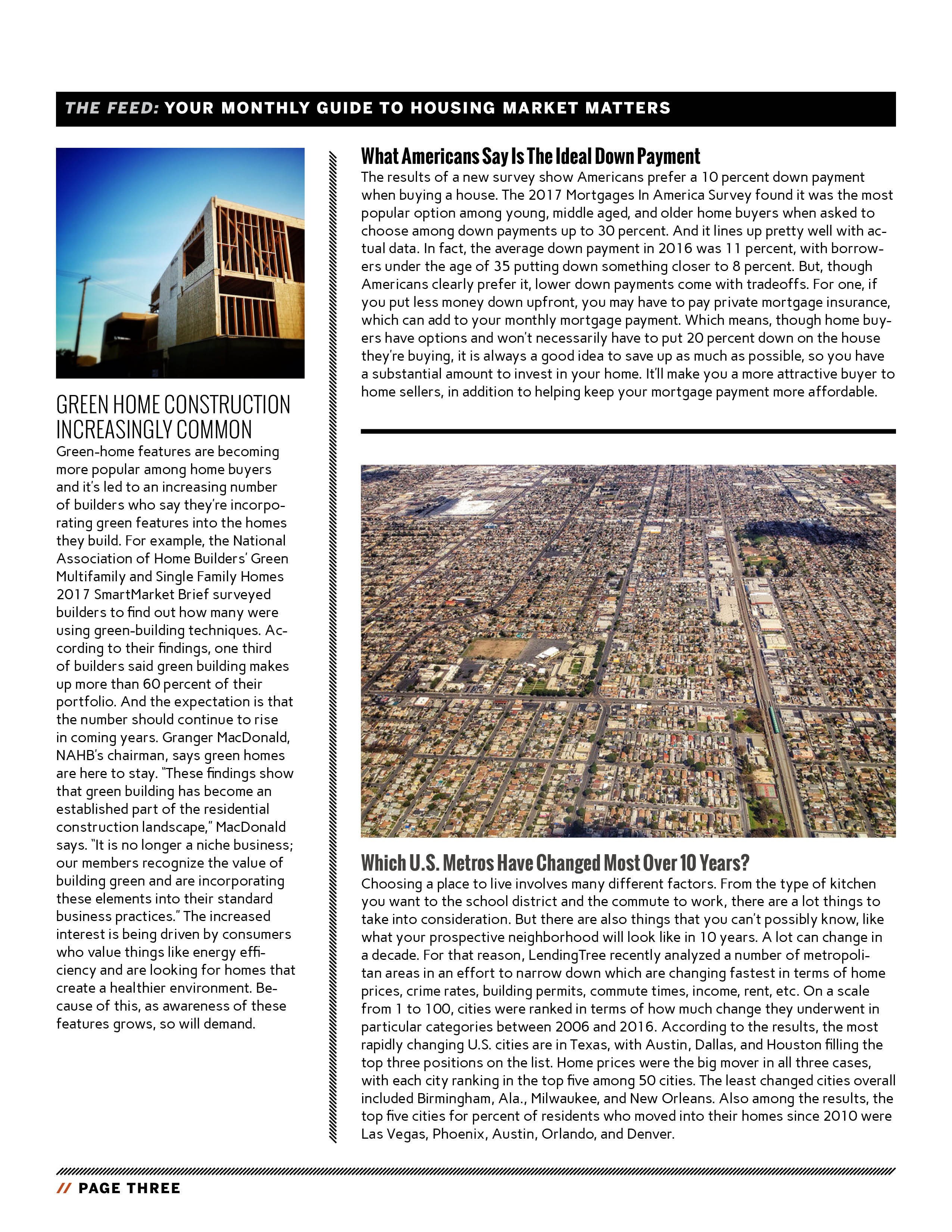

Income inequality is a hot topic these days. But what about housing market inequality? Well, a recent analysis looked at 50 of the largest metropolitan areas with an eye for which had the biggest city-wide disparity between high-end homes and the lowest-priced available homes. The results may surprise you. That’s because, the housing markets with the widest range between the high and low end of the market aren’t necessarily the markets that would immediately come to mind. In other words, cities like San Francisco – which features some of the country’s highest priced homes – were more equal than Midwestern cities where the cost of living is much lower. In fact, the number one most unequal housing market was Detroit, where the home values range from $32,000 to $431,000. Salt Lake City, on the other hand, was the most equal market, with median prices between $191,000 to $597,000. In this case, inequality might just be better for buyers. That’s because, the most unequal markets offer a wider range of prices for buyers to choose from, which means home buyers at all ends of the spectrum will have an easier time locating something that fits their budget. More here.

May Newsletter

Nearly 60% Of Homeowners Plan Home Improvements

If you’re a homeowner, you know the to-do list is never ending. And, if you’re a buyer, you’ll know soon enough. That’s because, owning a home means maintaining a home. Proof of that can be seen in the fifth annual LightStream Home Improvement Survey. According to the results, 58 percent of surveyed homeowners say they’re planning to spend money on home improvement projects in 2018. And the number who said they plan on spending $35,000 or more has doubled from last year. But though there are more homeowners planning projects this year, the list of projects hasn’t changed all that much. Once again, outdoor upgrades remain the most popular, with decks, patios, and landscape projects topping the list. Kitchen and bathroom remodels, of course, also rank high, coming second and third on Americans’ home improvement, to-do list. So how are these homeowners planning on paying for all these upgrades and renovations? Well, the vast majority said they were paying for their projects out of savings. However, another way homeowners are saving on their home improvement bills is by doing, at least, some of the work themselves. More here

If you’re a homeowner, you know the to-do list is never ending. And, if you’re a buyer, you’ll know soon enough. That’s because, owning a home means maintaining a home. Proof of that can be seen in the fifth annual LightStream Home Improvement Survey. According to the results, 58 percent of surveyed homeowners say they’re planning to spend money on home improvement projects in 2018. And the number who said they plan on spending $35,000 or more has doubled from last year. But though there are more homeowners planning projects this year, the list of projects hasn’t changed all that much. Once again, outdoor upgrades remain the most popular, with decks, patios, and landscape projects topping the list. Kitchen and bathroom remodels, of course, also rank high, coming second and third on Americans’ home improvement, to-do list. So how are these homeowners planning on paying for all these upgrades and renovations? Well, the vast majority said they were paying for their projects out of savings. However, another way homeowners are saving on their home improvement bills is by doing, at least, some of the work themselves. More here

Americans Feel Optimistic About Home Buying

An increasing number of Americans say they feel now is a good time to buy a house, according to the most recent Home Purchase Sentiment Index from Fannie Mae. The index – a monthly measure of how consumers feel about real estate, home prices, mortgage rates, job security, and their financial situation – is now nearing its all-time high, reached in September. Doug Duncan, Fannie Mae’s chief economist, says Americans’ perception of the real estate market is improving. “In November, the HPSI rebounded to near its all-time high, returning the index to its gradual upward trend and suggesting fairy stable consumer home-buying attitudes,” Duncan said. “These results are consistent with our expectation that the housing market will continue its modest expansion going forward.” Among respondents, there was a 7 percent increase in participants who said now was a good time to buy a house and a 4 percent increase in the number who feel it’s a good time to sell. More here.

Despite Price Spike, No Evidence Of Housing Bubble

Along with rising home prices, there has also been increasing concern that the housing market may be entering a bubble. And that’s not surprising, considering the housing crash is still fresh in peoples’ memories. So as home prices reach or exceed previous highs, potential buyers and current homeowners are naturally concerned about the possibility of another housing bubble and crash. According to a recent analysis from Freddie Mac, however, there is a pretty good reason to doubt that today’s price spikes are, in fact, evidence of an emerging bubble. Put simply, one of the primary reasons bubbles form is a perception that home prices will always rise. This causes investors to bid prices up and some mortgage lenders to offer easier credit. In short, a bubble isn’t real. Today’s price increases, on the other hand, are being driven by a lack of for-sale inventory and slower-than-normal new home construction. That means, it is more likely that prices aren’t being driven upward by irrational confidence but, instead, are being driven by an unbalanced market. “The evidence indicates there currently is no house price bubble in the U.S., despite the rapid increase of house prices over the last five years,” Freddie Mac’s chief economist Sean Becketti said. “However, the housing sector is significantly out of balance.” More here.

November Newsletter

New Home Sales Up 30% Over Last Year

New Home Sales Up 30% Over Last Year

In September, new home sales were 29.8 percent higher than they were at the same time last year, according to new numbers from the U.S. Census Bureau and the Department of Housing and Urban Development. The data shows sales up 3.1 percent from the month before and at their second-highest level since the recovery began. That’s good news for the housing market because any increase in new home sales helps spur more new home construction, which raises for-sale inventory and moderates price increases on all homes up for sale. As it is, the median price of a new home sold in September was $313,500; the average sales price was $377,700. And, with the number of new homes for sale lower than the month before, prices will likely continue to rise in the near term. Still a more favorable labor market and low mortgage rates have helped balance higher prices and kept buyer demand high. As an example, economists and analysts predicted a sales decline for September, making the results both unexpected and a good indication that potential home buyers aren’t being deterred by higher prices. More here.