The value of a particular house has to do with many different factors. The condition of the house, the location, the school district, supply, demand, and the surrounding neighborhood’s amenities are among some of the most well known. But a recent analysis has pinpointed another, less well known, factor that may help push prices upward. According to the study, areas that have stricter land-use regulations – such as density laws and permit review times – have seen much larger increases in home values compared to areas with less restrictive regulations. What does this mean? Well, it’s fairly simple. In areas where builders have a more difficult time building new homes because of local laws and procedures, fewer new homes get built. And, during times when there are a lower-than-normal number of existing homes available for sale, that can cause price increases to accelerate, as there will be more buyers than homes for sale. However, it’s important to note that the areas with the strictest land-use regulations also tend to be major coastal cities, where available lots are already hard to come by. In other words, there are a lot of factors that go into how a home is priced and the rate at which its value rises or falls. More here.

How Long Does It Take Renters To Save For A House?

With rental costs and home prices both increasing, it’s become more challenging for renters to save for a down payment. How much so? Well, according to one recent analysis, the typical renter will have to save for nearly six and a half years to come up with a 20 percent down payment on a median-priced home. And, since the median home value is currently $216,000, depending on your prospective neighborhood, it could take even longer to save up for a house. Renters who aspire to homeownership shouldn’t get discouraged, though. Despite the fact that a 20 percent down payment is the standard amount recommended by financial experts, it is not a requirement in order to buy a house. In fact, depending on the particular terms of your mortgage, you can put down as little as 3 percent. In 2017, for example, 29 percent of first-time buyers had a down payment between 3 and 9 percent. That’s why it’s important to explore your options before deciding homeownership is out of reach. More here.

Where Homeowners Have The Most Extra Cash

Your financial health isn’t really about how much money you make. It’s more about how much you have left over once you’ve paid all your bills. After all, if you make $1 million a month but also spend $1 million, you’re still struggling financially. And no one likes worrying about money. For that reason, a recent analysis took a look at the 50 biggest cities in the country and – based on household income, home prices, and cost of living – tried to determine where homeowners were able to live most comfortably. Fortunately, the results show that in 44 of the 50 cities included the average homeowner had money leftover at the end of the month. But surprisingly, the hardest places for Americans to put away a little extra cash weren’t necessarily the most expensive places to live. In fact, cities in the Midwest and South were among the toughest, rather than pricier areas on the coasts. For example, Detroit, Memphis, New Orleans, and Cleveland were four of the six cities where residents showed a negative balance. Philadelphia also made the list. The number one spot, however, was Miami, where a high cost of living and a low median income make it a tough place to save. More here.

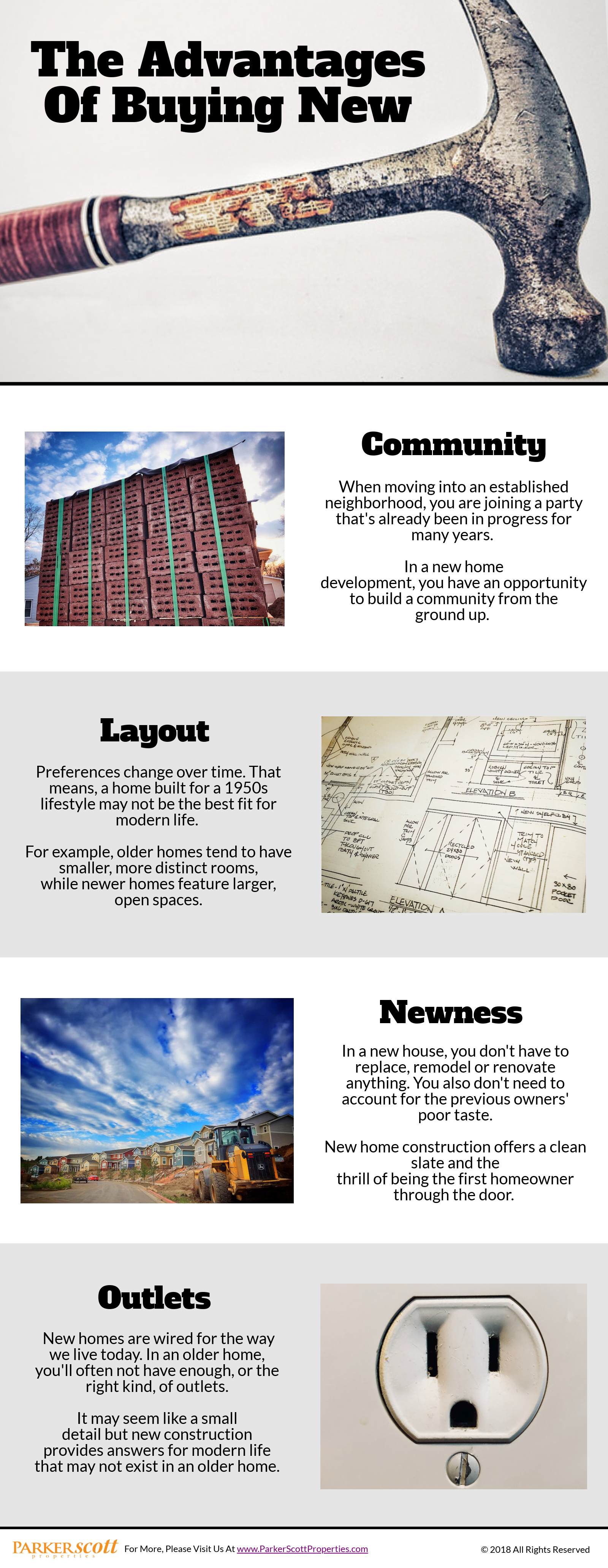

The Advantages Of Buying New

Your July Home Checklist

July Newsletter

20 Ideas for Easygoing Summer Parties

New Guyton Listing!!

How A Sellers’ Market Could Be Good For Buyers

The housing market is about supply and demand. When there are a lot of buyers and too few homes, prices and competition rise, making it a good time for homeowners who want to sell. When there are more homes than buyers, prices fall and bargains abound. In short, the market will usually favor either buyers or sellers. But, naturally, conditions that are good for buyers will lead to more buyers and vice versa. In other words, the pendulum swings back and forth. Which is why, a recent survey holds hope for buyers concerned about higher prices and increasing competition. The National Association of Realtors’ Housing Opportunities and Market Experience survey found that 75 percent of Americans think now is a good time to sell a home. And, if the perception that it’s a good time to sell leads to more homes being listed for sale, that will soon begin to moderate prices, making buying a more affordable proposition for the almost equal number of Americans who say they think now is a good time to buy. More here.

Generation Z May Become Homeowners Earlier

Generation Z – which is defined as people born between the mid-1990s and early 2000s – is quickly approaching adulthood and will soon face the decision of where to live and whether to rent or buy. But, according to a recent analysis, they may be facing challenges past generations didn’t. For example, the results of one study show that they will spend less time renting but will pay more than young people have in the past. With current median rent at $1,418 per month and rising, generation Z is expected to spend $226,000 on rent in their lifetime. That’s a lot. And it’s more than baby boomers or millennials spent. But despite that, generation Z is expected to become homeowners earlier than millennials have. One reason is the cyclical nature of the economy. Another is the fact that more than half say they considered buying before renting their current place. Also, they are just as likely as older generations to say they consider owning a home to be part of achieving the American Dream. In other words, if long-term economic trends hold up, the next generation of home buyers will have a better economy and job market to help fuel their dreams of homeownership. More here.