First-time home buyers are an important demographic when it comes to the health of the housing market. Because they’ve historically accounted for about 40 percent of home sales, they garner a lot of attention from experts, economists, and analysts hoping to gauge how the market is doing and where it’s headed. In recent years, first-time buyers have been less active than usual. The financial crash and recession led to a long period where Americans of typical home-buying age did not have the economic stability or job security to feel comfortable pursuing homeownership. Then, even after economic conditions began to improve, a lack of affordable, starter homes kept many younger Americans on the sidelines. This year, conditions are still challenging but new numbers from Freddie Mac show things may finally be changing. That’s because, first quarter results show that first-time buyers accounted for 46 percent of new mortgages during the early part of this year. That’s the largest quarterly share since 2012 and an indication that young Americans are finally becoming more active in the real-estate market. More here.

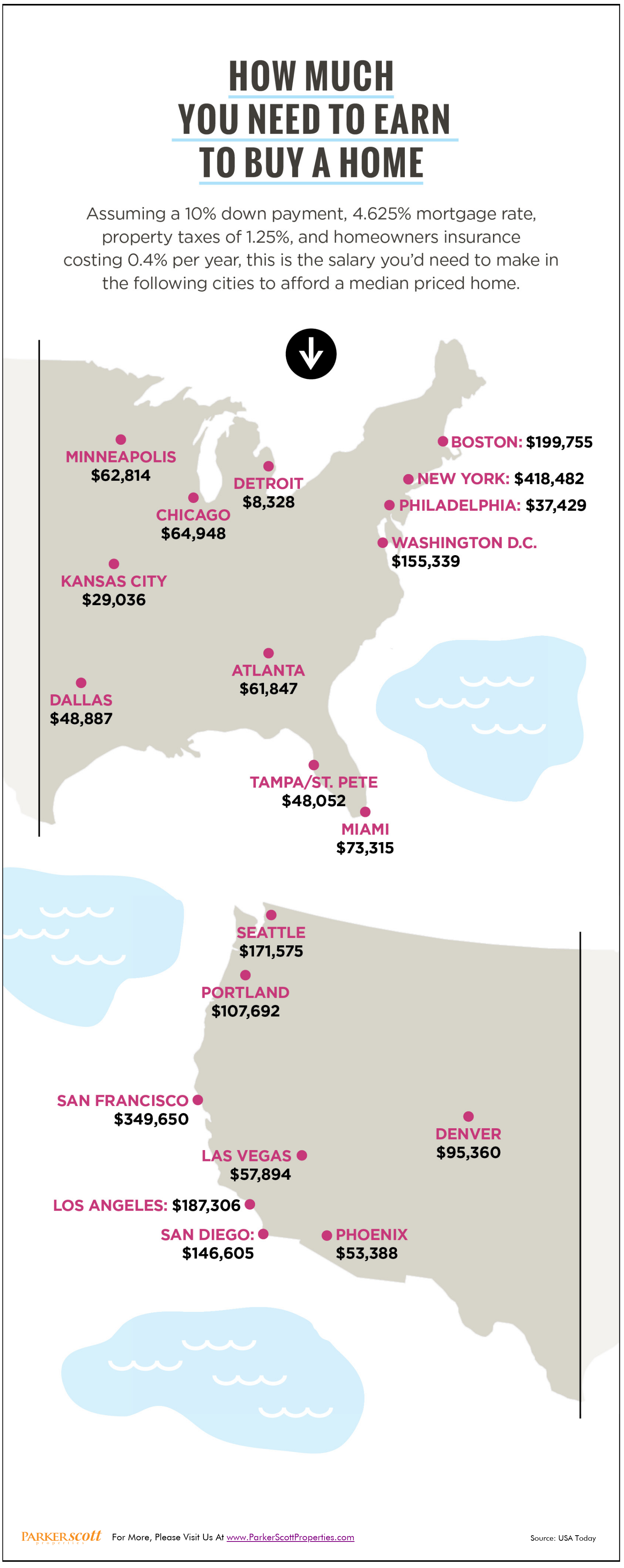

How Much You Need To Earn To Buy A Home

June 2018 Newsletter

Compromise Isn’t Just For Home Buyers

With buyer demand high and the number of houses for sale low, today’s market is favorable for homeowners who want to sell. But though they’re likely to find interested buyers, homeowners shouldn’t expect that everything will always go their way. In fact, a home’s sale almost always involves a negotiation and home sellers, just like buyers, should expect to have to compromise here and there. For example, 76 percent of sellers said they had to make at least one concession when selling their home, according to one recent survey. That means, even in markets that favor sellers, homeowners should have some flexibility when it comes to working out the details of the final sale. Home sellers should also be prepared to make some pre-sale improvements to their house, as the vast majority of recent home sellers also said they had to fix up their home before listing it. In short, regardless of how hot your local market is, you still have to get your house in shape and work with your home’s buyer to ensure the sale is a success on both ends. More here.

Housing Outlook Says Take The Long View

If you spend any time following the real estate market or economy, you know there’s no shortage of data. Nearly every day there’s a new report detailing some corner of our economic lives, whether it’s consumer spending, mortgage rates, jobs, or home sales. But reading the day-to-day news reports can sometimes give you a distorted view of what’s really happening. That’s because monthly updates on the housing market’s ups-and-downs can be more volatile than a look at annual results. And so it’s important to take a big-picture view of the market from time to time. For example, Fannie Mae’s most recent Economic and Housing Outlook says, despite a slower-than-expected first quarter, the economy will continue to grow. And, according to Doug Duncan, Fannie Mae’s chief economist, home sales will also continue to improve, despite a more challenging environment for buyers. “Soft residential investment last quarter should prove temporary, as home sales resume their slow upward grind, with inventory shortages playing friend to prices but foe to affordability and sales.” More here.

How Mortgage Rate Increases Affect Home Buyers

Mortgage rates have been increasing lately and there is an expectation that they will move higher this year. But while home prices get a lot of attention, rising mortgage rates are a little more difficult for buyers to calculate in terms of what it will cost them. Here’s some help. According to one recent model, a less than one percent increase in mortgage rates over the next year would result in a $100 increase to the typical monthly mortgage payment. But since the costs of homeownership are influenced by many different factors, this projection has to make certain assumptions about things like the rate at which home prices will increase, for example. In other words, any increase to mortgage rates will cost home buyers but just how much is difficult to calculate precisely. So what should home buyers expect? Well, since a stronger economy and improved job market make it more likely that the Fed will raise interest rates further this year, buyers should expect that mortgage rates will remain low by historical standards but continue to edge higher, taking monthly mortgage payments higher along with them. More here.

What Style Of House Do You Prefer?

Most regions offer house hunters a variety of architectural styles to choose from. Whether you prefer bungalows to ranches or modern over contemporary, you can likely find something that fits your preference. But, according to one recent survey, what you’re looking for might depend on your age. That’s because the results show millennial home buyers are looking for a different kind of home than older buyers. For example, younger buyers expressed a preference for colonial and contemporary homes, when they had a preference at all. On the other hand, buyers over the age of 55 were much more interested in finding a ranch – which is an architectural style favored by only 6 percent of millennials. Of course, some of this has to do with practicalities – such as retirees in search of a one-story home because it eliminates any concern about future mobility and navigating stairs – but it’s also a question of personal taste and aesthetics. Ultimately, though, whatever type of house Americans say they prefer, they generally all say they want that house to have ample storage, a garage, and multiple bedrooms. More here.

Are More New Houses On The Way?

Generally speaking, there are fewer homes available to buy right now than is considered normal. And though conditions will differ from one market to the next, when inventory is an issue, it leads to competition and higher prices. That’s because, there are too many buyers vying for the number of homes currently available. But when there are more buyers than there are homes for sale, conditions are also ripe for builders. And typically, they’ll take notice and build more homes to accommodate those buyers. Based on recent readings of the National Association of Home Builders’ Housing Market Index – which measures builders’ confidence in the market for new homes – that may be where the market is right now. For example, builders confidence has been at or above 70 for four consecutive months, on a scale where any number above 50 indicates more builders see conditions as good than poor. And most of their optimism is based on market conditions and their expectations for future sales, rather than current traffic. Which means, builders see an opportunity in this year’s market and may begin ramping up construction of new homes. If that happens, it’ll provide more choices for buyers and help slow spiking price increases. More here.

Single Home Buyers Face Added Challenges

Without the benefit of two incomes, single home buyers face some added challenges when looking to buy a house. For one, it takes longer to save for a down payment. In fact, according to a new analysis, married or partnered couples can save a 20 percent down payment on the typical home in less than five years. For single home buyers, it takes closer to 11 years. Add to that, single home buyers are more likely to be looking for a smaller, affordable home – which is precisely the type of house that is currently in highest demand. Zillow senior economist, Aaron Terrazas, says two incomes helps with savings but also with increasing the number of homes available to buy. “Single buyers typically have more limited budgets, which means they are likely competing for lower-priced homes that are in high demand,” Terrazas said. “Having two incomes allows buyers to compete in higher priced tiers where competition is not as stiff.” Of course, your individual financial situation and local market conditions will ultimately determine how much you’ll need to save and how much competition you’ll face for available homes. But single, married, or otherwise, it’s best to be as prepared as possible before heading out to look for a house to buy. More here.

Contracts To Buy Homes Rise For 3rd Straight Month

If you look at just about any reading of the current housing market, you’ll find that there are a lot of Americans interested in buying a home right now. Whether it’s because of pent-up demand that built up in the years following the housing crash or a drive to buy now while mortgage rates are still well below their historical norm, the fact is buyer demand is high. The most recent National Association of Realtors’ Pending Home Sales Index provides more evidence of this. That’s because the index – which measures the number of signed contracts to buy homes – ended the year with its third consecutive monthly increase. Lawrence Yun, NAR’s chief economist, says the housing market has started the year with a little bit of momentum. “Another month of modest increases in contract activity is evidence that the housing market has a small trace of momentum at the start of 2018,” Yun said. “Jobs are plentiful, wages are finally climbing and the prospect of higher mortgage rates are perhaps encouraging more aspiring buyers to begin their search now. More here.