America’s Most & Least Stressed Out Cities

As everyone knows, real estate is mostly about location. What $500,000 buys you in one neighborhood will be far different than what it affords you in another. Put another way, your money will go a lot farther in the Midwest than it will on the West Coast. Which is why a recent analysis showing a growing number of cities where the median home value is $1 million or more isn’t quite what it initially seems. Though it’s true that the number of million dollar cities has doubled over the past five years and that, within a year, there will likely be 23 more, a closer look at where these cities are will help explain the numbers. That’s because most of those new million dollar cities are located in areas that are already among the most expensive in the country. For example, more than half of the new metros added will be in the areas surrounding major cities like Los Angeles, New York, Seattle, and San Jose. Which means, while it still represents an increase in home values across the country, the growing number of million-dollar metros doesn’t necessarily reflect an acceleration in home price increases. More here.

You can tell a lot about the way an area grew by the age of its homes. The pace of suburban sprawl, for example, can be mapped just by observing the way homes get newer as you get further from the city’s center. Houses built in the 1920s give way to homes from the ’50s and ’60s and so on. But that’s not all you can learn from paying attention to the collective age of the country’s housing stock. You can also tell a lot about the housing market’s ups-and-downs. One example can be found in a recent analysis from the National Association of Home Builders. According to the NAHB, the median age of owner-occupied homes is now 37 years, which is up from 31 years in 2005. In fact, more than half of our homes were built before 1980 and 38 percent were built before 1970. In other words, America’s homes are getting older. But why? One reason is that there have been fewer new homes built over the past decade, mostly due to the housing crash and financial crisis. That has caused an increase in the median age of the housing stock. It also has caused a boost to the remodeling industry, as older homes require more renovations to keep up with new technology and features desired by home buyers. More here.

With rental costs and home prices both increasing, it’s become more challenging for renters to save for a down payment. How much so? Well, according to one recent analysis, the typical renter will have to save for nearly six and a half years to come up with a 20 percent down payment on a median-priced home. And, since the median home value is currently $216,000, depending on your prospective neighborhood, it could take even longer to save up for a house. Renters who aspire to homeownership shouldn’t get discouraged, though. Despite the fact that a 20 percent down payment is the standard amount recommended by financial experts, it is not a requirement in order to buy a house. In fact, depending on the particular terms of your mortgage, you can put down as little as 3 percent. In 2017, for example, 29 percent of first-time buyers had a down payment between 3 and 9 percent. That’s why it’s important to explore your options before deciding homeownership is out of reach. More here.

Home buyers this year have faced higher prices, more competition, and rising mortgage rates. In short, it’s been a challenging year. But that’s not to say it isn’t a good time to buy a house. There are many reasons to be optimistic about homeownership, in fact – and a few that put current conditions in perspective. Take mortgage rates, for example. According to Freddie Mac, the long term average is 8.16 percent, which means today’s rates are still low historically. Also, home equity is increasing. In fact, it’s up 13% year-over-year. And rising home equity means today’s homeowners are seeing their investment grow. There is also evidence that market conditions may begin to improve. For one, new home construction has been making gains and that means more homes for buyers to choose from. It also means buyers should begin to see prices moderate and competition wane, as more new homes are built to meet today’s high level of buyer demand. In short, there are a lot of good reasons to be optimistic about buying a house this year, despite market challenges. More here.

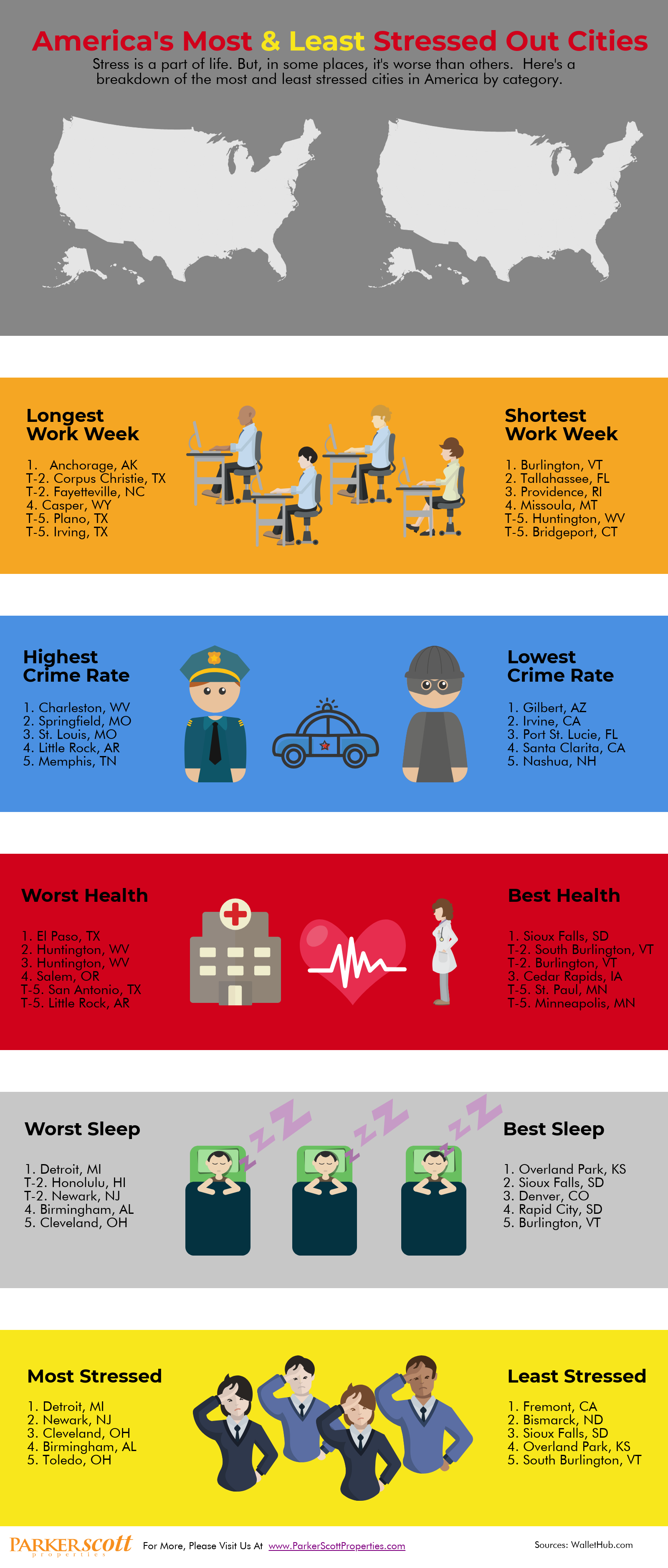

Your financial health isn’t really about how much money you make. It’s more about how much you have left over once you’ve paid all your bills. After all, if you make $1 million a month but also spend $1 million, you’re still struggling financially. And no one likes worrying about money. For that reason, a recent analysis took a look at the 50 biggest cities in the country and – based on household income, home prices, and cost of living – tried to determine where homeowners were able to live most comfortably. Fortunately, the results show that in 44 of the 50 cities included the average homeowner had money leftover at the end of the month. But surprisingly, the hardest places for Americans to put away a little extra cash weren’t necessarily the most expensive places to live. In fact, cities in the Midwest and South were among the toughest, rather than pricier areas on the coasts. For example, Detroit, Memphis, New Orleans, and Cleveland were four of the six cities where residents showed a negative balance. Philadelphia also made the list. The number one spot, however, was Miami, where a high cost of living and a low median income make it a tough place to save. More here.

If you were asked to name a hot home design trend, you probably wouldn’t guess log homes. And yet, new data from the National Association of Home Builders shows last year’s sales of log and timber homes were 56% higher than in 2012. That’s a big jump. So what’s behind the increase? Well, for one thing, today’s log and timber homes don’t resemble what might come to mind when thinking of an old-fashioned “log cabin.” According to the NAHB, “Revenues from log and timber frame homes have risen at a faster pace than units sold over the past six years as floorplans for the homes have expanded and offerings more extravagant.” In other words, today’s log homes are bigger and more luxurious than in the past. In fact, the average log home is 2,031 square feet. Still, the popularity of the homes is impressive when considering the fact that sales last year were only 7.8 percent below the number sold in 2006, while the rest of the single-family construction industry is down 42 percent. In short, log homes have been around forever and, based on their current popularity, they aren’t going anywhere any time soon. More here.

New homes are generally more expensive than existing homes. There are a couple of reasons for this. One is that everything in a new home is brand new and you’re going to pay a premium for that. This is really no different than paying more for an older home that’s recently undergone an extensive renovation. New things cost more than used things. The other reason new homes are generally higher priced is that builders, for the past several years, have been primarily building houses for the high-end of the market, due to the fact that there was more demand for new homes among luxury buyers following the housing crash. But new numbers from the U.S. Census Bureau and the Department of Housing and Urban Development should be good news for buyers who are interested in buying new but may not have a luxury-home budget. That’s because June’s new residential sales statistics show a 4.2 percent drop in the median sales price for new homes year-over-year. The median sales price is now $302,100. Surging new home sales between $200,000 and $299,000 were behind the decline, indicating an uptick in new homes available in more affordable price ranges. More here.