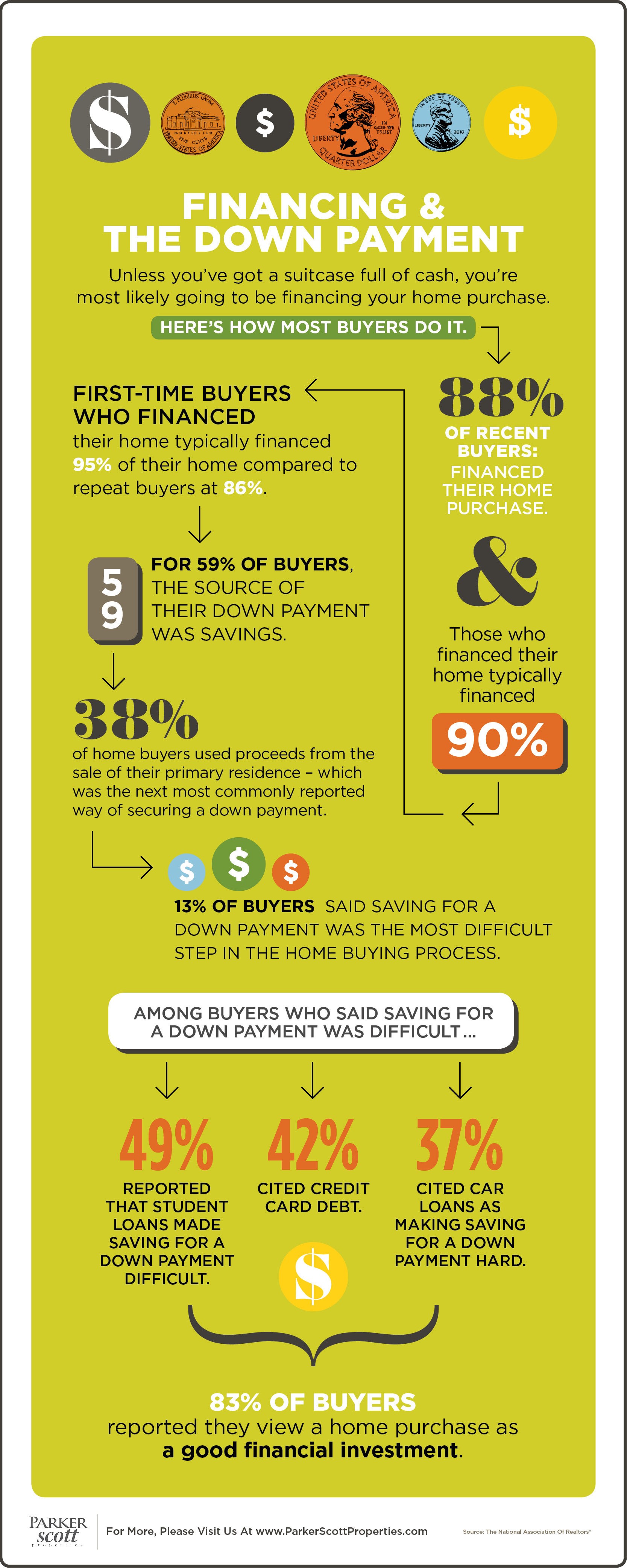

Financing & The Down Payment

Without the benefit of two incomes, single home buyers face some added challenges when looking to buy a house. For one, it takes longer to save for a down payment. In fact, according to a new analysis, married or partnered couples can save a 20 percent down payment on the typical home in less than five years. For single home buyers, it takes closer to 11 years. Add to that, single home buyers are more likely to be looking for a smaller, affordable home – which is precisely the type of house that is currently in highest demand. Zillow senior economist, Aaron Terrazas, says two incomes helps with savings but also with increasing the number of homes available to buy. “Single buyers typically have more limited budgets, which means they are likely competing for lower-priced homes that are in high demand,” Terrazas said. “Having two incomes allows buyers to compete in higher priced tiers where competition is not as stiff.” Of course, your individual financial situation and local market conditions will ultimately determine how much you’ll need to save and how much competition you’ll face for available homes. But single, married, or otherwise, it’s best to be as prepared as possible before heading out to look for a house to buy. More here.

It isn’t news that home prices have been headed upward for awhile now. And, according to the latest S&P Case-Shiller Home Price Indices, they are continuing to climb at around the same pace as they have been in recent months. Which is to say, the price increases haven’t yet slowed. Of course, how quickly prices are increasing depends on where you’re looking to buy. Large metropolitan areas – and especially those in the West – are seeing the sharpest increases, while the price gains are more muted in the Midwest. But, no matter where you are, the best way to prepare for higher prices is to know what you want, what you can afford, and where your limits are. In competitive and higher priced markets, having a firm idea of what you can spend and where you’ll compromise will make it less likely that you’ll end up going over budget because of a bidding war or buying more house than you can comfortably afford. Making sure you’re prepared before heading out to look at homes also means securing financing in advance, so you’ll be ready to make an offer when you find a home you love. More here.

Potential home buyers often describe the home buying process as being complicated. And, most likely, a lot of their confusion stems from the financing side of the transaction. A lack of knowledge about what is required and how to proceed can cause otherwise qualified borrowers to become intimidated and even delay their dreams of homeownership. For example, prospective buyers often have misconceptions about down payment requirements, believing they are required to put down much more than is actually necessary. And, though calculating the size of your down payment depends on a number of factors, believing that you can’t buy a house with less than a 20 percent down payment can be enough to convince a potential home buyer that they aren’t yet ready to buy. That’s why it’s important to contact your lender to explore your options before you talk yourself out of buying. Though there is plenty of information available online – and recent research shows the internet is the primary source of information about mortgages – you can’t get an accurate appraisal of your options and price range without the help of a qualified professional. Don’t allow misconceptions to hold you back from buying the home of your dreams. More here.

Along with rising home prices, there has also been increasing concern that the housing market may be entering a bubble. And that’s not surprising, considering the housing crash is still fresh in peoples’ memories. So as home prices reach or exceed previous highs, potential buyers and current homeowners are naturally concerned about the possibility of another housing bubble and crash. According to a recent analysis from Freddie Mac, however, there is a pretty good reason to doubt that today’s price spikes are, in fact, evidence of an emerging bubble. Put simply, one of the primary reasons bubbles form is a perception that home prices will always rise. This causes investors to bid prices up and some mortgage lenders to offer easier credit. In short, a bubble isn’t real. Today’s price increases, on the other hand, are being driven by a lack of for-sale inventory and slower-than-normal new home construction. That means, it is more likely that prices aren’t being driven upward by irrational confidence but, instead, are being driven by an unbalanced market. “The evidence indicates there currently is no house price bubble in the U.S., despite the rapid increase of house prices over the last five years,” Freddie Mac’s chief economist Sean Becketti said. “However, the housing sector is significantly out of balance.” More here.

This year’s real-estate market has been a mixed bag. On the one hand, demand from home buyers has been strong and an increasing number of renters say they hope to one day own a home. But though there has been strong demand from buyers, there has been a lack of homes available for sale in many markets. Low inventory has caused home prices to continuing rising and sales – though higher than the year before – to fall below expectations considering the level of demand from potential buyers. So what’s in store for next year? Well, Lawrence Yun, the National Association of Realtors’ chief economist, sees improvement. According to Yun, continued economic gains should lead to more home sales and more new home construction. However, because for-sale inventory will remain a concern, Yun is cautiously optimistic. “An overwhelming majority of renters want to own a home in the future and believe it is part of their American Dream,” Yun said. “Assuming there are no changes to the tax code that hurt homeownership, the gradually expanding economy and continued job creation should set the stage for a more meaningful increase in home sales in 2018.” More here.

Recent data from Fannie Mae shows a large majority of current renters intend to one day buy a house. In fact, just 18 percent of surveyed renters said they plan to remain renters forever. So what are some of the obstacles renters face when thinking about whether or not they should begin taking steps toward homeownership? Well, the upfront costs of buying a home were the top answer, with 45 percent of respondents citing coming up with money for a down payment and closing costs as the obstacle that keeps them from buying. However, an almost equal amount said they were most concerned about their credit. Other answers included insufficient income, too much debt, confusion about the buying process, and job security. In short, current renters want to buy but are worried they aren’t financially secure enough to become homeowners. And, though that is a legitimate concern, Fannie Mae also points out that their pervious research has shown many potential home buyers overestimate the size of the down payment they’ll need and are unaware of many of the programs available to help first-time home buyers reach their goal of becoming homeowners. More here.

A new survey from the National Association of Realtors shows Americans are optimistic about their economic situation and increasingly think now is a good time to buy or sell a home. The quarterly survey found a spike in both the number of current renters who think now is a good time to buy a house and homeowners who say it’s a good time to list their house. In fact, among current homeowners, the number who said it was a good time to sell hit a record high. Lawrence Yun, NAR’s chief economist, says the optimism is largely driven by economic conditions. “Jobs are plentiful, wage growth is finally showing signs of life, home values are up considerably in the past five years and the stock market is at record highs,” Yun said. “The economy is not perfect, and growth overall is still sluggish, but the financial health of the typical household looks as healthy as it has since the recession.” The survey’s results also show increasing positivity among Americans about their personal financial situation and their outlook for the next six months. More here.

American homeowners may be overestimating their home’s worth, according to new data. The research shows appraisals in August were 1.35 percent lower than homeowners expected. There are a couple of reasons this could be happening. First, there has been a lot of attention paid recently to how far prices have risen over the past few years. But, while this is true, it is not necessarily true in every neighborhood, in every city, across the country. So, homeowners who have been hearing that prices are going up, may have a misperception of just how much their home’s value has risen. As evidence of this, data shows homeowners in the West thought their homes would appraise for less than what they eventually did, while homeowners in the Midwest were disappointed to find their appraisals didn’t meet their expectations. Another possible reason for the misperception is that homeowners are generally attached to their homes. And, if you’ve invested time, money, and maintenance into a property, when it comes time to sell or refinance, you’re naturally going to – not only hope for the best possible outcome – but expect that everyone else who looks at your house will see it the way you do and value you it just as much. Unfortunately, though, that may not always be the case. More here.