Sales Trail Hot Summer Housing Market

The National Association Of Realtors’ most recent Pending Home Sales Index shows that the hot summer housing market has not deterred hopeful home buyers from looking for a house to buy. But though there is a high level of demand from buyers, supply issues continue to hold back sales numbers. In fact, the index found that the number of contracts to buy homes signed in May was essentially flat from the month before. Lawrence Yun, NAR’s chief economist, says sales are being hurt by low inventory but recent news that new home construction hit a 10-year high should be encouraging to prospective buyers. “Several would-be buyers this spring were kept out of the market because of supply and affordability constraints,” Yun said. “The healthy economy and job market should keep many of them actively looking to buy, and any rise in inventory would certainly help them find a home.” Regionally, results were mixed, with the Midwest, Northeast, and West all seeing modest increases, while the South saw a 3.5 percent drop. Pending home sales numbers are an important indicator, as they cover contract signings and not closings, which means they often foreshadow upcoming sales data. More here.

20 Ideas for Easygoing Summer Parties

New Guyton Listing!!

The Rising Cost Of Renting A Home

When debating whether to rent or buy your next place, the argument in favor of renting usually includes the fact that it’ll be cheaper – especially since you don’t have to pay for closing costs or save for a down payment. However, renting a place isn’t all that cheap these days and, depending on what you’re looking for, prices may be rising even faster than expected. According to recently released data, rental rates are increasing and particularly among two and three-bedroom homes. In fact, rental homes, generally, are climbing in price faster than apartments. Nationally, a typical two-bedroom now costs $1,310 per month and the cost for a typical three-bedroom is up to $1,445. And, depending on your local market, it could be even higher. So why is rent rising faster for homes than it is for apartments? Well, for some of the same reasons home prices are climbing. For one, new, and smaller, apartments are the focus of most rental unit construction, while the supply of single-family homes to rent is mostly fixed. More here.

How To Keep Your House Cool This Summer

How A Sellers’ Market Could Be Good For Buyers

The housing market is about supply and demand. When there are a lot of buyers and too few homes, prices and competition rise, making it a good time for homeowners who want to sell. When there are more homes than buyers, prices fall and bargains abound. In short, the market will usually favor either buyers or sellers. But, naturally, conditions that are good for buyers will lead to more buyers and vice versa. In other words, the pendulum swings back and forth. Which is why, a recent survey holds hope for buyers concerned about higher prices and increasing competition. The National Association of Realtors’ Housing Opportunities and Market Experience survey found that 75 percent of Americans think now is a good time to sell a home. And, if the perception that it’s a good time to sell leads to more homes being listed for sale, that will soon begin to moderate prices, making buying a more affordable proposition for the almost equal number of Americans who say they think now is a good time to buy. More here.

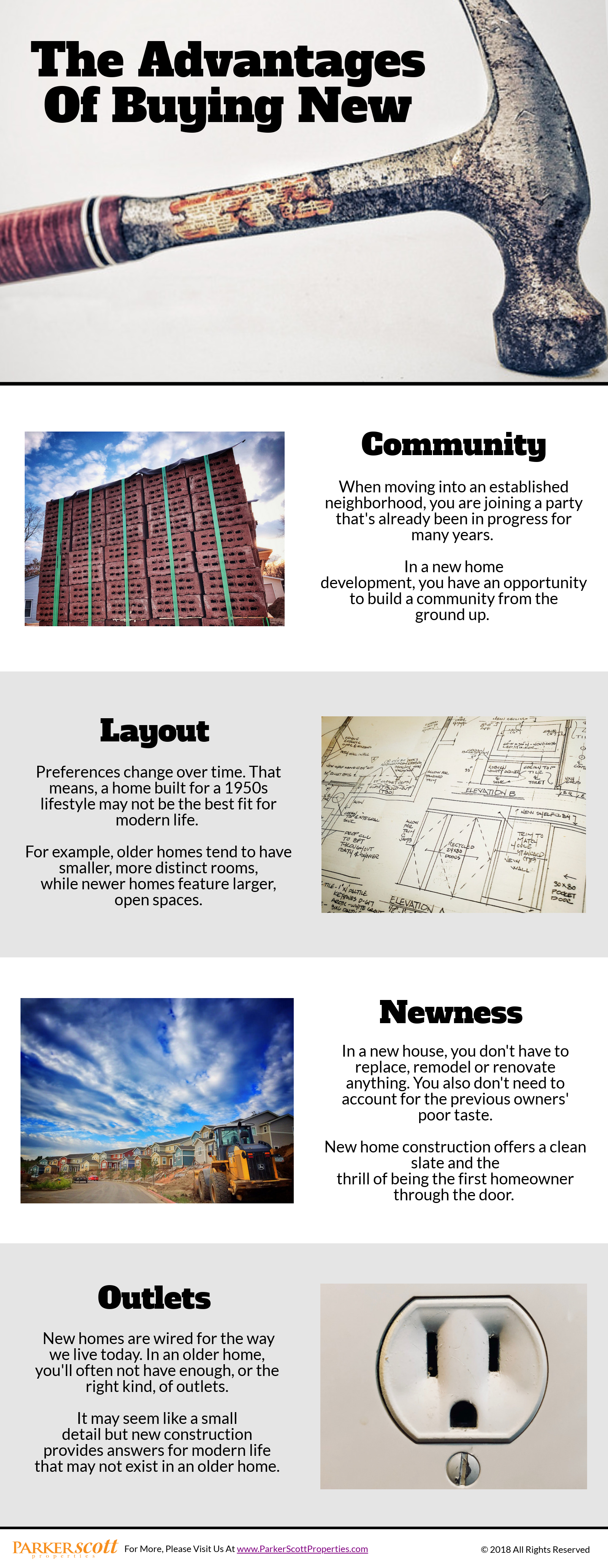

The Advantages Of Buying New

What Do Homeowners Do With Their Equity?

One of the main arguments in favor of buying a home is equity. When you rent, you’re sending your monthly payment to a landlord. As a buyer, your monthly mortgage payment is helping to build equity. Of course, many homeowners wait and then, following the sale of their house, use their accumulated equity to help buy their next home. But you can also use a home equity loan to access the value your home has accrued. So what do homeowners who take home equity loans do with the money? Well, a recent survey asked borrowers and came up with an answer. Not surprisingly, the top reason homeowners took out loans was to fund home improvement or remodeling projects. This is a common strategy since taking out a loan to improve your house means you may be able to recoup some of the cost if, and when, you sell the home. Other common answers included money to invest in another property, emergency expenses, retirement funds, and debt consolidation. More here.

Cautious Buyers May Be Overestimating Costs

Affordability is the top concern for potential home buyers entering the summer season. That’s not a surprise. With prices and mortgage rates up, it’s natural that Americans who are hoping to buy might be leery when seeing news of rising housing costs. But, though affordability conditions are challenging in some markets, buyers may have some misconceptions that are adding unnecessary stress and anxiety. For example, according to the results of one recent survey, potential home buyers see saving for a down payment as the biggest obstacle preventing them from buying a house. But, at the same time, they overestimate the amount of money they’ll need to put down in order to buy. The survey found 58 percent of participants said they are planning for a 20 percent down payment. But though that may be the recommended down payment amount, it isn’t required. The National Association of Realtors, for example, found that the median down payment for first-time buyers has been at 6 percent for the past three years. In other words, though home buyers are right to take seriously the costs and responsibilities of becoming a homeowner, they may want to explore all of their options before deciding they can’t afford to buy. More here.